The following is a reprint of Statement 3, Maintaining Low Inflation and Strong Growth, from Budget Paper No. 1: Budget Strategy and Outlook 2000-01.

Statement 3: Maintaining Low Inflation

and Strong Growth

Part I: Introduction

Australia is entering the new millennium with the introduction of a modern taxation system which will sustain the economy’s longer-term growth potential. The New Tax System will provide more robust taxing arrangements for both Commonwealth and State Governments. It will lead to more efficient investment decisions throughout the economy, with significantly reduced business costs; and Australians will keep a higher proportion of their before-tax earnings, providing greater incentives to work and save.

As with all significant advances, there will be an adjustment process but this will quickly give way to visible lasting benefits.

There will be a one-off increase in consumer prices when The New Tax System is introduced. This price effect will not endanger the combination of strong growth and low inflation that has been achieved over the last few years. Competition should ensure that price adjustments associated with The New Tax System do not re-ignite inflation; and there will be no need for employees to seek higher wages because the generous compensation package will boost their real after-tax incomes.

The New Tax System is being introduced at a time of strong competition and dynamic markets. These have not come about by accident. Rather, they are the result of deliberate policy action, pursued at both the macro and microeconomic levels. Credible medium-term monetary and fiscal policy frameworks have provided the stable and supportive investment climate to ensure that Australian businesses take full advantage of the wide range of structural reforms that have been pursued.

Increased competition and more dynamic markets have contributed to lifting the medium-term potential growth rate of the Australian economy to around 3 to 4 per cent per annum. This means that the rate of growth that the Australian economy can sustain without producing significant inflationary pressures is now above the average rates of growth achieved during the past three decades.

The benefits of sustained strong economic growth are already evident with the unemployment rate around the lowest in almost a decade. If this strong growth is to be sustained, the current macroeconomic policy framework and the ongoing structural reform agenda must be maintained, including the implementation of The New Tax System. In these circumstances, there would be the opportunity to drive the unemployment rate much lower still, potentially to its lowest level for more than a quarter of a century.

Part II: The Benefits of Tax Reform

The implementation of The New Tax System is a major reform that will bring both more robust government finances and substantial efficiency gains throughout the economy. The main features of The New Tax System are the abolition of a range of inefficient indirect taxes and the introduction of a goods and services tax (GST), significant personal income tax cuts, reforms to social security benefits and reforms to Commonwealth-State financial relations.

Narrowly Based Inefficient Indirect Taxes Replaced with a Broadly Based GST

A GST will be introduced from 1 July 2000 to replace the Wholesale Sales Tax (WST) and a range of inefficient State taxes, such as accommodation taxes (on 1 July 2000), Financial Institutions Duty (FID) and stamp duties on marketable securities (on 1 July 2001) and debits tax (by 1 July 2005, subject to a review by the Ministerial Council for Commonwealth State Financial Relations). The Ministerial Council will also review the need for retention of a range of other business stamp duties by 2005.

Cost Reductions for Producers

The removal of the existing inefficient indirect taxes will significantly reduce business costs. This is because these taxes become embedded in the cost structures of business (see Box 1), imposing a hidden burden on Australian exporters and import competing businesses in particular. Over half of the existing WST is paid as tax on inputs used by businesses. These embedded taxes also cascade, as the tax paid by businesses becomes embedded in the price on which WST subsequently becomes payable further down the chain. The existing tax system discriminates against manufactured goods, while favouring service industries on which WST is not payable.

Less Distorted Relative Prices Increase Allocative Efficiency

In contrast to WST, the GST is not a cascading tax. GST registered businesses at each stage of the production chain receive a credit for the GST paid on inputs at earlier stages of production. The effect is that the GST imposes a uniform 10 per cent effective tax rate on taxable supplies to final consumers. This effective tax rate does not vary according to the production chain involved and applies to taxable supplies of both goods and services.

Providing the States with a More Secure and Growing Revenue Source

The introduction of The New Tax System provides for the transfer of all GST revenues to the States and Territories, affording them a stable and growing source of revenue. Access to the GST revenues will allow the States and Territories to abolish a range of narrowly based indirect taxes that impede economic growth. It will also remove their reliance on financial assistance grants and revenue replacement payments from the Commonwealth.

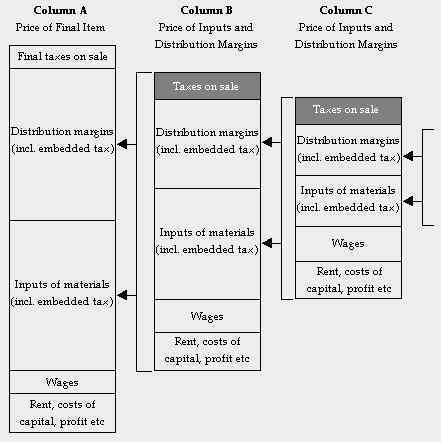

Box 1: Embedded Taxes The final prices of all goods and services (commodities) can be split into production costs (such as wages and the cost of materials), distribution margins (such as transport costs and wholesale and retail margins), capital costs (such as rent, interest and a profit margin) and indirect taxes (Column A). However, the distribution margins and cost of materials, along with some capital costs, may include an indirect tax component (Column B). The industries in Column B may also have paid indirect taxes on their inputs or their distribution margins and so on (Column C,…). Since all of these ‘hidden’ taxes (denoted by the shaded boxes) are embedded in the final price of the item shown in Column A they are appropriately described as ‘embedded’.

The prices of most goods and services contain at least some element of embedded taxes. Under The New Tax System, the WST and several other cascading taxes will be abolished. This will reduce the cost of producing these items, regardless of whether the final item is currently taxed or not. Competition, along with Australian Competition and Consumer Commission (ACCC) monitoring (discussed in Part III), will ensure that these savings are passed on to consumers. |

GST revenue will be distributed to the States and Territories according to horizontal fiscal equalisation principles. These principles take into account differences in the capacities of the States and Territories to raise revenue and in their expenditure requirements to ensure that a

ll jurisdictions have a broadly equal capacity to provide an average standard of government services (see Budget Paper No. 3).

Lower Effective Marginal Tax Rates and Improved Work Incentives

Reductions in personal income tax, increases in family assistance and assistance for low income and older Australians will ensure that low and middle income people, in particular, will keep a higher proportion of their before-tax earnings, providing greater rewards and incentives to work and save. These changes will see significant reductions in effective marginal tax rates faced by many low and middle income families, which have been a disincentive to workforce participation.

Lower Income Tax Compliance Costs

The New Tax System replaces all existing income tax collection and reporting systems, including Pay As You Earn (PAYE), prescribed payment system (PPS), reportable payments system (RPS), provisional tax and company instalments, with one new, comprehensive Pay As You Go (PAYG) system.

It will be a flexible system with taxpayer obligations transparent and easily managed as a by-product of other business activities. In this way, paying income tax and collecting other taxes will become simpler and less costly.

Under PAYG, both individuals and companies will pay tax on their business income at the same time. PAYG will make it possible for business to make one net payment, or to claim one net refund, quarterly and will abolish provisional tax and the uplift factor.

Individuals who now pay provisional tax will benefit from these changes in many cases since, unlike provisional tax, PAYG instalments will be paid after income has been earned and will be based on actual income. Companies will pay tax earlier than now, but a deferral of company instalments due for the 1999-2000 year after PAYG commences will assist companies to adjust to the new arrangements.

The Government has also introduced the Australian Business Number (ABN) as a single business identifier. The ABN will facilitate the introduction of a single tax compliance statement and streamline business interaction between taxpayers and the Commonwealth.

Benefits Enhanced by Business Tax Reform

The New Tax System reforms will be enhanced by the improvements to business tax arrangements that were announced as part of The New Business Tax System. Key elements of The New Business Tax System are a lower rate of company tax (reduced from 36 per cent to 30 per cent over two years) and reduced capital gains tax. The New Business Tax System will provide Australia with an internationally competitive business tax regime.

Part III: Competition and Indirect Tax Reform

The New Tax System is being introduced into a highly competitive environment. This environment will be fundamental to ensuring that the full benefits of The New Tax System flow throughout the economy and that the combination of strong growth and low inflation is maintained.

Prices and Competitive Markets

The Australian economy is reaping the rewards of a broad agenda of structural reforms. A common goal of many of these reforms is increased competition and improved market dynamism (see Box 2). As a consequence, competition in the Australian economy is now much stronger than it has been at any time in the post-war period.

One characteristic of a competitive market is that purchasers can readily choose between a range of sellers to find the best combination of quality and price. In such a market, the most successful sellers are those who best judge market conditions when setting their prices. Those who set excessive prices are forced to pull their prices into line or risk losing business. Competition drives dynamism because the speed of change in offering alternatives to the customer is of fundamental importance. The competitive nature of markets for most goods and services in Australia today means that vigorous, dynamic competition is now the driving force behind market prices.

Competitive markets have a range of other benefits. On the supply side, producers wishing to increase their profitability are forced to focus on alternatives to charging higher prices. For example, they may seek to reduce their costs, find more efficient and innovative production methods or pursue new markets. Australian businesses are proving that they can respond to competition by continuously improving their performance in all of these ways.

Demand side factors have also added to competitive pressures in Australian markets. For example, firms that have improved their marketing techniques have made it easier for consumers to compare quality and price, thus making markets even more competitive. Increased consumer awareness and ‘shopping around’ have played an important part in the transformation of the Australian economy to one characterised by highly competitive markets. This trend will continue as new technologies, such as the internet and e-commerce, make consumers better informed and further reduce the effective distance between consumers and potential suppliers.

As well as these direct benefits, competition improves the efficiency of the use of resources, including the allocation of those resources across sectors. (See Box 2 for more details.)

Box 2: Reforms Promoting Competition and Market Dynamism A wide range of economic reforms has transformed the Australian economy. These reforms have increased competition and helped to create more efficient and dynamic markets. They have also helped to increase the capacity of the Australian economy to respond to new opportunities and challenges. The New Tax System is part of this ongoing reform agenda and will deliver significant efficiency benefits to the marketplace by replacing a range of narrowly based indirect taxes with a broadly based GST. This will reduce the distortion of production and consumption choices by differing tax treatments. Other significant reforms are catalogued below.

The increased competition and more dynamic markets resulting from these reforms are benefiting consumers, exporters and other businesses.

|

The direct impact of increased competition on prices is most easily seen in those sectors where significant structural reforms have taken place, such as telecommunications and electricity. The marked impact that increased competition has had on prices in these industries is noted in Box 3.

Box 3: Examples of Increased Competition Affecting Prices The effect of increased competition on prices is evident in the key sectors of telecommunications and electricity.

Significantly, the benefits of competition in these industries extend beyond the immediate consumers of these services. Telecommunications and electricity are essential inputs to many other sectors. Price reductions in these services constitute a reduction in the costs of other businesses, enhancing their competitiveness. These cost reductions in turn cascade through to other businesses and final consumers. |

A broader indicator of the degree of competition in the tradable sector of the Australian economy is the ratio of gross trade (imports plus exports) to GDP, which provides a measure of trade intensity. Chart 1 highlights the increase in competition that has occurred since the mid-1980s. During the 25 years to 1984, trade intensity rose only slowly from close to 20 per cent of GDP to around 25 per cent. In contrast, the increase in trade intensity over the past 15 years has been much greater, as can be seen in the steeper trend over this period in Chart 1.

Chart 1: Trade Intensity(a)

(a) Trade intensity is exports plus imports relative to GDP.

Source: ABS Cat. No. 5206.0 and Treasury.

The Interaction of Tax Reform and Competition

As noted above, the highly competitive environment in which The New Tax System is being introduced will put pressure on excessive prices and maximise the benefits to consumers.

The indirect tax changes associated with the introduction of The New Tax System mean that most individual prices will change. The price impact will vary from item to item, with some prices rising, some falling and some unchanged. These relative price changes must occur to bring about the more efficient allocation of resources flowing from the more neutral (less distorting) indirect tax system.

The ACCC has been monitoring the early stages of The New Tax System implementation. So far, the ACCC has monitored the reduction in WST on a range of goods from 32 per cent to 22 per cent on 29 July 1999 and the cigarette excise changes on 1 November 1999. The ACCC has reported that both the actual decline in prices to consumers, following the reduction in WST, and the increase in cigarette prices compared favourably with their prior calculations. Extrapolating from this experience provides the basis for confidence that price rises will not be excessive and that cost reductions will flow through as the remaining elements of The New Tax System take effect.

A further example is provided by the recent behaviour of car prices. The replacement of the existing WST on cars with the GST means that new car prices will be significantly lower than otherwise under The New Tax System. Although the tax changes have not yet occurred, competition has meant that car prices have already fallen considerably in anticipation of The New Tax System.

These examples suggest that the highly competitive environment will resolve most concerns about price exploitatio

n and also prevent businesses trying to use the tax changes as an excuse to raise prices or rebuild margins. Firms that have been under pressure to squeeze their margins or seek cost reductions due to competition before the introduction of the GST will continue to face the same competitive pressures under The New Tax System.

While competition will be fundamental to limiting price rises in the transition to The New Tax System, the ACCC will monitor price changes to provide a safety net against excessive price increases. The ACCC has been given strong powers under the Trade Practices Act 1974 to monitor prices and prevent price exploitation during The New Tax System transition period. There are substantial penalties if profiteering is proven.

The ACCC has already undertaken extensive price surveys across metropolitan and regional Australia to ensure that businesses do not unreasonably raise prices in anticipation of the GST implementation date. It expects to continue this extensive survey activity throughout the transitional period, which expires on 1 July 2002.

Part IV: Tax Cuts and Compensation Measures

The New Tax System contains measures that negate the overall price effects of indirect tax reform on people’s incomes. The income package comprises three distinct elements: reductions in personal income tax; increases in family assistance; and assistance for low income and older Australians. The measures are estimated to cost $17 billion in a full year, an amount equivalent to 20 per cent of the Commonwealth’s individual income tax collections in the year prior to tax reform.

These measures more than compensate for price effects as they ensure that disposable incomes will increase by more than the likely increase in prices implied by the changes to the indirect tax arrangements. The generous nature of the measures means that there is no justification for employees to seek higher wages because of the introduction of The New Tax System. This supports the assessment that the change in Australia’s tax arrangements will not re-ignite inflationary pressures.

When assessing the adequacy of these measures, it is important to focus on 1999-2000 and 2000-01 as a whole, rather than just the CPI outcome for the September quarter 2000 in isolation. As set out in Part V below, the impact of the revised indirect tax arrangements on prices will not be felt evenly through 2000-01. The increase in the CPI in the September quarter 2000 will be followed by several quarters where prices will increase by less than would otherwise have been the case. This means that any attempt to assess the adequacy of the compensation package against the increase in the CPI in the September quarter alone, will necessarily be misleading.

Personal Income Tax Marginal Statutory Rates

Commencing from 1 July 2000, reductions in personal tax will be delivered through an increase in the tax-free threshold and reductions in marginal tax rates at a cost of $12 billion per year. The existing and new tax scales are set out in Table 1.

Table 1: Income Tax Scales

An indication of the extent to which the reductions in personal tax will increase take-home pay is shown in Chart 2. The chart shows the annual increase in average wages after adjusting for changes in personal tax rates and the effect of The New Tax System on prices in 2000-01. Average real after-tax wages are estimated to increase by around 3 per cent in 2000-01, compared with an average increase of a little below 2 per cent per annum over the previous four years. The estimate for 2000-01 reflects modest growth in real wages (adjusted for ongoing inflation), supplemented by a net reduction in tax flowing from The New Tax System of around 2 percentage points.

Chart 2: Annual Growth in Real After-tax Average Wages(a)

(a) Real average after-tax wages are defined as average earnings (national accounts basis) adjusted using statutory income tax rates (including the Medicare levy) divided by the CPI.

(b)Includes forecasts for the March and June quarters 2000.

Source: Treasury.

Families

Changes to family assistance under The New Tax System will greatly advantage families by increasing rates of assistance, addressing ‘poverty traps’ and simplifying the number of available benefits. Over 2 million families will benefit from increased assistance of $2.4 billion a year, from 2000-01.

The private health insurance initiative came into effect on 1 January 1999 and provides Australians who are members of private health funds with a 30 per cent benefit on the cost of their health insurance contributions as either a rebate on tax, a direct payment, or as an up-front premium reduction. In 2000-01 the cost of this measure is expected to be around $1.9 billion.

Pensioners and Allowees

As part of The New Tax System, the maximum rates of all allowances and pensions will be increased by 4 per cent from 1 July 2000. For pensioners, the 4 per cent increase will be paid as a pension supplement on top of the base pension. The base pension will continue to be underpinned by the Government’s legislative commitment to maintain the single rate of pension of at least 25 per cent of Male Total Average Weekly Earnings.

The 4 per cent increase to pensions and allowances is comprised of an advance of 2 per cent for future indexation adjustments, and a real increase of 2 per cent above what the pension would have otherwise been with normal indexation. This arrangement will ensure that allowees and pensioners will be 2 per cent better off than they otherwise would have been, regardless of the effect of indirect tax reform on prices.

Other associated allowances, such as the pharmaceutical allowance and the mobility allowance, will also increase by 4 per cent from 1 July 2000. The maximum rate of rent assistance will increase by 7 per cent. The income test-free areas for allowances and pensions will increase by 2 per cent, as will the pension asset test-free areas.

The pension withdrawal rate with respect to income will be reduced from 50 per cent to 40 per cent.

The Pensioner Rebate (and the Low Income Aged Persons Rebate) will be increased by a further $250 a year for single age pensioners and $175 a year for each of an age pensioner couple, above the amounts which ensure that full-rate pensioners are freed from income tax.

The combined cost of these measures is around $2 billion a year.

Many senior Australians will also benefit from one-off savings bonuses that are designed to help maintain the value of their savings, following the introduction of the GST. The value of the bonuses is expected to be around $1 billion.

| Box 4: The Impact of Compensation Table&nb

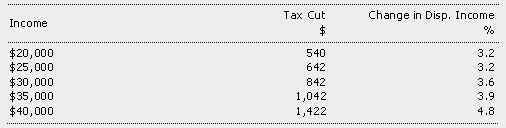

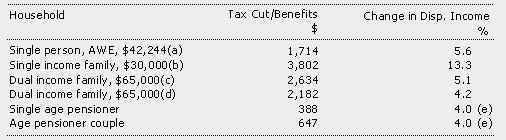

Table 2: Tax Cuts

Table 3 below, provides an indication of the impact of tax reform measures on disposable income for a number of representative income units. The table shows that the increases in income more than offset the expected first year impact on prices of The New Tax System of 2 per cent and are significantly greater than the longer run impact of 1 per cent. While demonstrating that each of these groups gain from tax reform, the table highlights the significant gains that accrue, in particular, to single income families. Pensioners and allowees will receive a one-off increase in benefits of 4 per cent on 1 July 2000, in addition to twice yearly indexation. Table 3: Tax Cuts and Other Benefits — Households

(a) Annual equivalent of ABS Trend AWE, Persons, Total Earnings, Full-time Adult, March quarter 2000 of $810.20 per week (ABS Cat. 6301.0). This shows the compensation to be provided consequent on the introduction of The New Tax System. This will ensure that pensioners and allowees will be 2 per cent better off than they would otherwise have been. In addition to this one-off compensation, pensions and allowances will also be increased on the normal indexation days in September 2000 and March 2001. |

Part V: The Timing of the Price Changes

As noted previously, the highly competitive nature of the Australian economy, combined with the generous compensation arrangements integral to the tax reform package, lead to the conclusion that price changes due to indirect tax reform should be one-off in nature, and hence not feed into ongoing inflation. It is this conclusion that underlies the assumptions and expectations of the timing effects of the price changes discussed below.3

Short Run Price Estimates

As noted in Statement 2, ‘ongoing’ inflation (that is, leaving aside the one-off impact of indirect tax reform on prices) is expected to be within the 2-3 per cent target band in 2000-01. In other words, the indirect tax changes are being implemented at a time when the outlook for ongoing inflation remains favourable.

The price changes associated with The New Tax System will not all occur on 1 July 2000, when the GST is introduced and the WST is abolished. For example, some parts of the overall package have already been implemented. The government’s 30 per cent rebate on private health insurance was introduced on 1 January 1999, the rate of WST on a range of goods was cut from 32 per cent to 22 per cent from 29 July 1999 and the new cigarette excise arrangements took effect from 1 November 1999. Other elements of The New Tax System will not come into effect until 2001, 2002 and 2005.

Nor will changes in retail prices necessarily occur at the time that the relevant indirect tax rates change. For example, there is some evidence that motor vehicle prices have already been affected, ahead of the introduction of the new tax arrangements. There has also been very strong activity in the housing sector ahead of the changes to the indirect tax arrangements that has seen prices of new project homes increase.

Taking these factors into account, the changes to indirect tax arrangements are estimated to increase the CPI by around 2 per cent during the year to the June quarter 2001. The impact on the CPI will become smaller over subsequent years as later elements of the package take effect.

The impact of the revised indirect tax arrangements on prices will not be felt evenly through 2000-01. The main impact will occur in the September quarter 2000 (see Chart 3), because the immediate impact of the GST on retail prices will only be partially offset by the removal of WST on final consumption items. While estimating quarterly outcomes is inherently difficult, the overall increase in the CPI in the September quarter could be of the order of 4 per cent, of which a little over 3 per cent would be the result of one-off price changes associated with indirect tax reform.

In the following couple of quarters, CPI increases will be smaller than would otherwise have been the case, as the removal of embedded WST and lower business costs (including from lower transport costs) restrain price increases at the retail level. While the exact timing effects may be complicated since competitive forces may result in businesses anticipating cost savings in their underlying cost structures, it is likely that CPI increases will be very low in the December quarter 2000 and the March quarter 2001.

Chart 3: Forecasts and Projections of the Impact

of The New Tax System

(a) Excludes the impact of The New Tax System on prices.

Source: ABS Cat. No. 6401.0 and Treasury.

This pattern of price increases underlies the forecast that the CPI will rise by 5 per cent in year-average terms in 2000-01 and by 5 per cent through the year to the June quarter 2001. This through-the-year increase comprises ongoing inflation of around 2 per cent and a one-off increase, due to the first year impact of the changed indirect tax arrangements, of around 2 per cent.

By the September quarter 2001, the through-the-year increase in the CPI is expected to fall to around 1 per cent, somewhat below the ‘ongoing’ inflation rate.

Long Run Price Estimates

The longer-term impact of The New Tax System on the CPI will be less than the impact in 2000-01. This is because other parts of The New Tax System package that will reduce the overall CPI impact (such as the phased introduction of input tax credits for motor vehicles and the abolition of various State taxes), will be introduced in 2001, 2002 and 2005. In the longer term, the overall effect of The New Tax System measures on the CPI is likely to be around 2 per cent, or around 1 per cent if tobacco is excluded.

In the original announcement of A New Tax System, the impact on the CPI given prominence was an increase of 1.9 per cent. Since that figure was first published, there have been changes to both the package itself and how the CPI is measured.

The original 1.9 per cent rise referred to the cumulative impact of the package on the CPI through the first tw

o years to 2001-02 and excluded the impact of the reforms on tobacco. Tobacco was excluded since the increase in tobacco excises reflects public health considerations, rather than indirect tax reform per se.

Over time, the impact of A New Tax System on the CPI was expected to fall below 1.9 per cent as businesses gained access to full input credits on their motor vehicle purchases, reducing business costs and hence ultimately consumer prices. As a result, the original long-run estimate of the CPI impact from A New Tax System was 1 per cent.

Since the original announcement, the package has been amended to make basic food GST-free, thus reducing the CPI impact. However, this change will be partly offset by increased business compliance costs associated with changes to the package and the changes to diesel fuel credit arrangements. The basic food exemption and other changes together are expected to subtract about percentage point from the cumulative CPI impact of the package. This would imply a cumulative CPI impact of around 1 per cent over the long run.

Another, more technical, factor that has affected the original estimate of the impact of indirect tax reform on the CPI is a change in how the Australian Bureau of Statistics measures the CPI. The change in the treatment of the First Home Owners Scheme, together with other changes made in calculating the CPI for the 13th series (as compared to the 12th series), will add around percentage point to the measured impact of The New Tax System.

Consequently, the long-run impact of tax reform on the CPI (excluding tobacco) remains around 1 per cent.

Part VI: Prolonging the Expansion

With ongoing inflation remaining at low levels, Australia has the opportunity to prolong the current economic expansion and push unemployment to around its lowest rate in over a quarter of a century.

Grasping this opportunity will require maintaining the Government’s economic policy framework and ongoing reform agenda. Implementation of The New Tax System is an important input to this outcome.

Australia’s economic policy framework is motivated by the objective of achieving a sustained increase in our growth rate, which would in turn allow higher incomes, stronger employment growth and lower unemployment. This framework should facilitate — not hinder — the sharing of these economic benefits across society in a sustainable manner. The economic reforms that have been implemented, and are underway, have lifted Australia’s potential growth to 3 to 4 per cent. As such, we have the prospect of sustained strong economic and employment growth (see Chart 4), which will lead to further inroads into unemployment.

Chart 4: Prolonging Growth and Increasing Employment

(a) Includes forecasts for the March and June quarters 2000.

Source: Treasury.

In previous decades, Australian economic performance has been periodically constrained by the emergence of macroeconomic imbalances, such as debilitating inflation and unsustainable current account deficits, following periods of strong economic growth, and despite unemployment remaining high. On occasions, macroeconomic policy settings allowed, or even contributed to, the emergence of excess demand pressures. In other cases, these imbalances may have resulted from the behaviour of participants in the private economy — such as through excessive wage claims.

Structural deficiencies meant that the economy did not have the flexibility and dynamism to prevent those imbalances emerging or to allow the economy to grow at its full potential. The subsequent policy tightening required to address the particular imbalance contributed to a downturn in economic growth and a ratcheting up of structural unemployment. For example, the monetary policy tightening utilised to address the impact of strong domestic demand on the current account deficit in the late 1980s resulted in negative economic growth in 1990-91 and sharply higher unemployment.

The economic policy framework now has clear objectives set in a medium-term context and aimed at lifting the growth potential of the economy. Fiscal and monetary policies are directed at keeping economic growth at a strong but sustainable rate, with a stable environment for saving and investing. Structural reform policies are directed at raising the economy’s growth capacity over time and reducing the rate of unemployment that can be achieved without threatening inflation. (See 1999-2000 Budget Paper No. 1, Statement 3 for details.)

While structural reform can provide the potential for the economy to achieve higher sustainable growth rates and for unemployment to fall further, achieving the economy’s full potential over coming years will depend on avoiding the short-term imbalances and subsequent policy responses that have ended past expansions. For example, it is crucial that excessive wages growth be avoided. This was a key factor in the development of imbalances during the mid-1970s and early 1980s that led to a tightening of monetary policy, truncating economic expansion and halting the process of reducing unemployment.

Structural reforms are reducing the risk that inappropriate aggregate wage increases will play a leading role in ending the current economic expansion. In particular, reforms to workplace relations have placed greater emphasis on negotiating employment arrangements at the enterprise level, and contributed to improved productivity and relatively stable real unit labour costs.

- These changes have also reduced the likelihood that wage outcomes achieved in former ‘leading wage’ sectors will be transmitted to the rest of the economy.

- The more competitive business environment that exists today has greatly reduced the opportunity for firms to pass on higher labour costs to the consumer.

As discussed in Statement 2, wages growth is expected to remain moderate during 2000-01, despite some pick-up, and the unemployment rate is expected to fall further.

As the unemployment rate declines, labour market pressures may exert a larger influence over wage outcomes than in recent years. However, there have been shortages of skilled labour in some areas, including information technology and telecommunications and selected skilled trades, for some time without aggravating aggregate wages outcomes. While labour pressures may intensify in some sectors and regions, there appears to be little evidence to suggest that there will be a deterioration in the availability of labour over the forecast period that could generate excessive wages growth across the economy.

There is no justification for employees to seek higher wage outcomes in response to the indirect tax changes as the personal income tax cuts provided in the tax package more than offset the price effects of the changed indirect tax arrangements (see discussion in Part IV). There is little evidence to suggest that the introduction of the indirect tax changes will have a significant impact on wage negotiations, although there may well be instances where employees seek to highlight these issues.

While some prominence has been given to enterprise agreements that include clauses related to the introduction of the indirect tax changes — such as the Toyota certified agreement — these clauses do not

appear to be widespread. Only around 4 per cent of employees covered by enterprise agreements signed in 1999 appear to have GST-related clauses.

On the basis of the outlook for wages, and the assessment of risks surrounding that outlook, wages growth is not expected to endanger the current economic expansion.

If a policy response were required to address excessive wages growth, it would threaten the continuation of one of the longest and strongest periods of robust economic growth in post-war Australia, as shown in Chart 5. This in turn would undermine the significant fall in the unemployment rate achieved in recent years, and could once again lead to a ratcheting up of unemployment.

Chart 5: Prolonging the Expansion

Source: Treasury.

Chart 6 indicates that unemployment has tended to increase rapidly during economic downturns and decline much more slowly during periods of economic growth. Provided the current macroeconomic policy framework and the ongoing structural reform agenda are sustained, including the implementation of The New Tax System, the continuation of the current economic expansion could be expected to offer a unique opportunity — some years hence — to again achieve and sustain an unemployment rate not seen in Australia for at least a quarter of a century.

Chart 6: The Unemployment Rate

Source: ABS Cat. No. 6202.0 and Treasury.

If the current expansion were prematurely ended by policy being needed to respond to excessive wages growth, this exciting prospect would be put at risk. It is important that participants in the economy understand the significant potential costs of unwarranted wage outcomes.

There is much at stake for Australia over the next few years. The current economic environment, including strong competition and an enhanced productivity performance, provides the potential for a significant improvement in the well being of all Australians through continuing strong and sustainable economic growth and reductions in unemployment. The introduction of The New Tax System is an important element in coming to this conclusion.

1 Communications Research Unit (Department of Communications, Information Technology and the Arts) and Phonechoice website (www.phonechoice.com.au).

2 Treasury estimates based on Electricity Supply Association of Australia Electricity Australia (various issues).

3 These estimates are based on detailed modelling involving assumptions regarding margins, flow through, etc. As such, the estimates cannot be improved after the event and hence will not be changed.